机构洞察:美国银行欧元外汇观点

美国银行 - 美元世界中的欧元

关键要点

贸易不确定性和货币政策让我们在短期内对欧元保持谨慎。我们看好欧元兑日元和欧元兑加元的下行。

但我们也担心欧元区的看跌情绪正在“过度”,一些头寸将变得脆弱。

看跌结果可能会迫使看涨行动。我们认为法国存在欧元下行风险,但德国和欧盟范围内的改革将带来上行风险。

短期看跌欧元,但除此之外存在上行风险

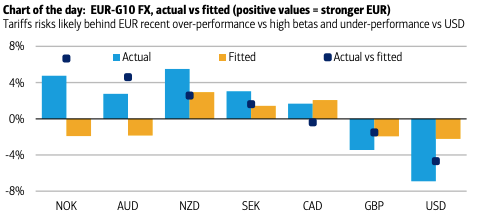

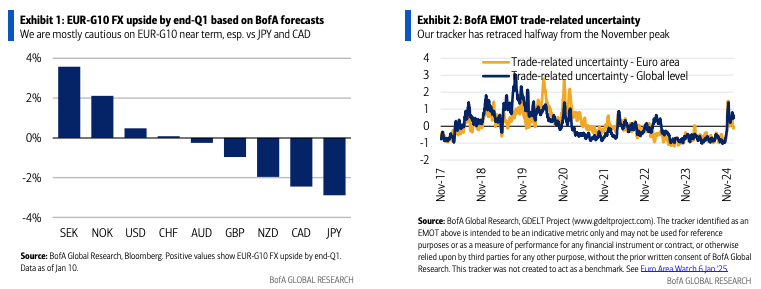

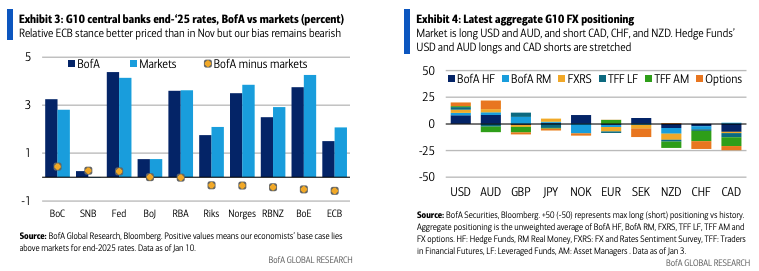

潜在的更高贸易不确定性和相对货币政策让我们在短期内对欧元保持谨慎。但我们也担心欧元区的看跌情绪正在“过度”,一些头寸可能会受到挤压。欧元兑日元走低仍然是我们看跌欧元的首选。我们也看好欧元兑加元的下行,部分原因是我们的量化信号。法国继续构成欧元下行风险,但我们认为德国财政政策重新考虑和欧盟范围内的改革主要带来上行风险。我们认为,过于悲观的欧元区结果可能会迫使采取急需的、可能改变游戏规则的行动。因此,虽然我们目前保持谨慎,但我们认为欧元区的悲观情绪是有限的。 短期内看跌欧元,因贸易不确定性和相对货币政策 我们对短期内欧元兑 G10 外汇持谨慎态度(图表 1),因为:(1)贸易不确定性可能上升,风险情绪恶化;(2)相对货币政策,尤其是在 12 月就业报告稳健之后(见 2025 年 1 月 10 日美联储观察)。我们认为,贸易不确定性已经解释了欧元兑美元表现不佳和欧元兑“高贝塔 G10”表现优异的很大一部分原因(见每日图表),至少基于典型的宏观驱动因素(货币政策、风险情绪、大宗商品价格)。但我们的追踪器显示,贸易不确定性已从 11 月的峰值回落(图表 2)。我们的经济学家确实发现,在美国12月非农就业数据公布之前,欧洲央行的定价是合理的(见25年1月6日欧元区观察),但他们的偏见仍然看跌(图表3),在风险调整后和相对于美联储方面更是如此。

EUR-JPY remains our preferred bearish EUR expression

• EUR-JPY remains our preferred bearish EUR expression. We remain short EUR-JPY via a ERKO put (strike: 158.75, down/out European barrier: 150, expiry May 23 2025, entry spot: 160.65, entry cost: 0.7425% EUR; current spot ref: 161.74, current cost: 0.67% EUR; risks to the trade are German fiscal stimulus and/or EA reforms, more hawkish ECB, or dovish BoJ – for our open and recently closed trades please see Global FX Weekly 10 Jan '25). On JPY, markets could start pricing in policy response should its weakness extend: 160 seems a key USD-JPY level to us (see Japan Watch 9 Jan '25).

• EUR-USD is slightly below our end-Q1 1.03 forecast. We see risks for more USD strength in the short term, on the Fed being done and on US tariffs after the inauguration (see also Global FX Weekly 10 Jan '25). But with the market short EURUSD (Exhibit 4) and Hedge Funds very short, we also see vulnerabilities unless/until Real Money clients step in (see USD Watch 6 Jan '25 and LCBF 7 Jan '25). We find USD’s relatively restrained reaction post-December payrolls suggestive (see US Watch 10 Jan '25).

• EUR-GBP: Our bias remains bearish. We are inclined to fade its recent move but prefer to wait for the market to turn short GBP from neutral (again Exhibit 4 and see also UK Viewpoint: The Great British Sell Off, 9 Jan '25).

•Antipodeans: EUR-AUD is around our end-Q1 forecast, but the long AUD positioning, esp. for Hedge Funds (Exhibit 4), and AUD’s greater reliance on CNY and China (see Global FX weekly 30 Aug '24) pose upside risks. By contrast, we see limited EUR-NZD upside, also given positioning (see World at a Glance 7 Jan '25).

• EUR-CAD: Our quant signals suggest downside near term risks (see FX Vol Insight 10 Jan '25), and so do positioning (Exhibit 4) and relative monetary policy (Exhibit 3), also given the strong Canadian labour market data (Canada Watch 10 Jan '25). • EUR-CHF: We maintain a bearish CHF bias incl. vs EUR, but for now we prefer to express it vs USD (see FX Vol Insight 10 Jan '25 and CHF Watch 7 Jan '25).

免责声明:提供的材料仅供参考,不应视为投资建议。 本文中表达的观点,信息或观点仅属于作者,而不属于作者的雇主,组织,委员会或其他团体或个人或公司。

过去的业绩不代表未来的结果。

高风险警告:差价合约(CFD)是复杂的工具,由于杠杆作用,存在快速亏损的高风险。 当与Tickmill UK Ltd和Tickmill Europe Ltd进行差价合约交易时,分别有69%和73%的零售投资者账户亏损。 您应该考虑自己是否了解差价合约的工作原理,以及是否有具有承受损失资金的的高风险的能力。

期货和期权:保证金交易期货和期权具有高风险,可能导致损失超过您的初始投资。这些产品并不适合所有投资者。请确保您完全了解这些风险,并采取适当的措施来管理您的风险。