NFP preview: aiming for a strong comeback, in order to increase chances for extension of Fed’s “pause”

After the slight job growth in May of just 75K, investors believe that US labor market will utilize its unexploited potential in June, gaining 160K jobs. At the last meeting, Powell hinted that Fed keeps tab on three-month trend in the data, rather than on the separate month prints, and if 160K consensus is confirmed, then the average for three months will be slightly higher than the previous one.

In addition to rebound in payrolls, wage growth is also expected to increase from May. Also, attention will be shifted on the U6 unemployment metric, which fell to a cyclical minimum in May, and the level of labor force participation, which will help track changes in the number of demotivated workers. In accordance with the Fed’s increasing emphasis on incoming data to determine the monetary policy path, the unemployment report may lead to two scenarios of the July meeting: an extension of the “patience period” in case of material gains in jobs and wages or increase in the odds of 50 bp rate cut in case the jobs market drifts away from projections strongly. If the data comes in line (especially in terms of jobs and wage growth), expectations about 25 bp rate cut is likely to remain in place.

Goldman Sachs expects job growth at 175K in June which should be roughly in line with the average rate over the past six months. Also, the bank dismisses a possibility of the impact of bad weather and Mississippi flood on job creation, stating that weak data for May was a combination of a slowdown in demand and seasonal constraints in supply. The last factor often put pressure on the May figures, especially when there was a shortage of labor in the market, which is still present. In this case, the inflow of students and graduates may ensure stable rates of hiring for several consecutive months.

If the report shows that job creation has significantly exceeded expectations, this will be a classic example of “bad good news” for the stock market, which rally banked on expectations of aggressive Fed’s easing, which may be under question in case of upside surprise in the data.

Why we can expect strong NFP?

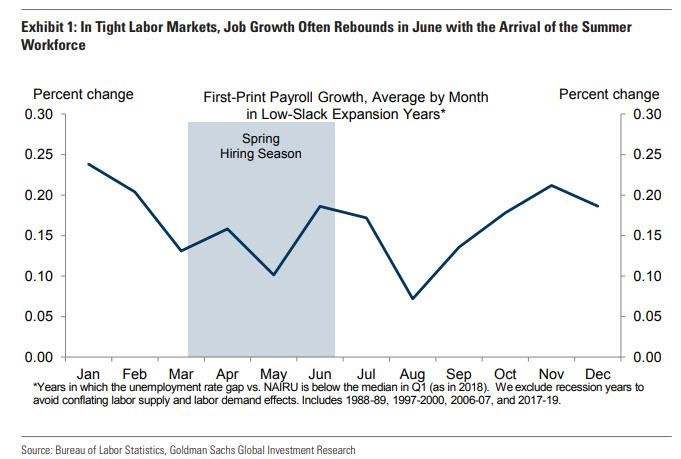

Seasonality. Goldman Sachs does not believe that the labor market reached a state of full employment and it was the shortage of workers that affected the pace of job creation in May. Here is the chart that shows that during the years of expansion (= tight labor market), the slowdown in job’s creation in May was replaced by an acceleration of growth in June:

This may reflect the trend of flooding the labor market in the first month of summer with students and graduates (the supply is pulled up to demand, providing increased job creation), as well as the transfer of employment plans by some firms to the beginning of the year, before the spring deficit in May (a kind of self-fulfilling prophecy). According to the data from previous months, some sectors grew well at the beginning of the year (in terms of jobs) before they slowed down growth:

- education and health care - + 58K average for January-April, + 27K in May;

- hotel industry and entertainment - + 35K average for January-April, + 27K in May.

Public education. It is expected that the decline in jobs from this sector in May by 14K will be offset by growth in June (jobs change in this sector demonstrates mean-reverting behavior).

Other indicators. Unemployment claims in June which remain at a historic minimum also hint on strong NFP as well as surveys of firms in the service sector. Although they indicated a slight cooling of activity, they show the willingness of firms to maintain healthy employment rates.

Among the arguments for weak NFP we can cite a negative surprise from ADP yesterday (+ 102K), weakening of PMI indices in the manufacturing sector, including the employment component (-1.2 points to 53.6 points), and the uncertainty associated with tariffs for Mexican goods (which could have caused some companies postpone plans to hire workers).

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.