Institutional Insights: Goldmans Sachs - Uncertainty, FOMC & Gold

.jpeg)

Institutional Insights: Goldmans Sachs – Uncertainty, FOMC & Gold

Markets closed on a weaker note as geopolitical tensions escalated. Prediction markets now suggest a 60-70% probability of US military action against Iran before July (Polymarket | US military action against Iran before July?), which may be an overreaction but reflects the prevailing sentiment. The US is showcasing significant military strength, with the USS Nimitz joining the USS Carl Vinson Carrier Strike Group, marking a rare dual-carrier presence in the region. BBC Verify reports that at least 30 US tanker aircraft have been relocated to Europe in the past three days to support bomber and fighter jet operations. While no confirmed US involvement has surfaced yet, markets remain on edge. A de-escalation following an initial show of force would be a favourable outcome.

Oil prices surged nearly 5% again yesterday, driven by CTA positioning, investor indifference, and a substantial 10 million barrel draw in API data (DOE data due this afternoon). Energy markets are now the primary channel for transmitting geopolitical risk.

In autos, there are signs of front-loading. Japan's exports declined in May for the first time in eight months, with auto shipments hit by tariffs. Similarly, US headline retail sales missed expectations, with auto sales dropping 3.9%, reversing prior front-loading trends. However, the core retail sales figures came in stronger. On inflation, import prices were revised higher, and GIR now tracks May core PCE at 0.18%, up from 0.14%.

Today’s primary focus is on the Fed. Rates are expected to remain unchanged, but adjustments are anticipated: GDP projections could be revised lower, while inflation forecasts may edge higher. The debate centers on the 2025 dot plot—some predict it will rise (indicating just one rate cut), while others expect it to remain flat. While there was hope for a dovish tone from Powell, given softer inflation and jobs data, he is likely to stay noncommittal during the press conference, given uncertainties around tariffs and Q2 GDP tracking at +4%.

US technicals remain supportive, with yesterday’s dip bringing the market back into gamma-heavy zones. Geopolitical uncertainty persists, and despite the market's eagerness for a resolution, a swift outcome seems improbable. Equities are beginning to price in tail risks, with SPX 1-month normalised risk/reversal trading at the higher end of its 52-week range and the spot VIX back at 21.6, despite the 15-day realised volatility on SPX at 15. The most likely scenario is that tensions remain contained but linger. With the US holiday tomorrow, attention will be on Powell and the FOMC.

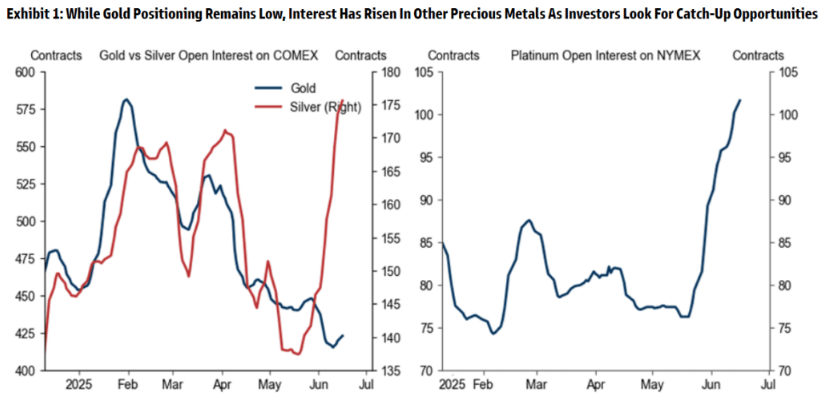

Side note: Surprising to see Gold open interest remains low.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!